In today’s increasingly connected world, people are studying, working, traveling, and relocating across borders more than ever before. Whether you are an international student, an expatriate professional, a frequent traveler, or a digital nomad, having the right international insurance policy is essential. It protects you from unexpected financial risks and ensures peace of mind wherever you are in the world. However, choosing the best international insurance policy can feel overwhelming due to the wide range of options available. This guide simplifies the process and helps you make an informed decision.

What Is International Insurance?

International insurance is a policy designed to provide coverage across multiple countries rather than being limited to one nation. Unlike domestic insurance, it accounts for varying healthcare systems, legal requirements, and living costs in different regions. Common types of international insurance include health insurance, travel insurance, life insurance, and property insurance. Among these, international health insurance is the most widely sought, as medical emergencies can be extremely costly abroad.

Why International Insurance Matters

Healthcare costs differ significantly from country to country, and in many destinations, treatment for non-residents can be expensive. Without adequate coverage, even a minor medical issue can lead to substantial out-of-pocket expenses. International insurance also helps with access to quality healthcare, emergency evacuation, repatriation, and sometimes coverage for routine check-ups. Beyond health, certain policies also offer protection against travel disruptions, loss of belongings, and personal liability, making them a comprehensive safety net.

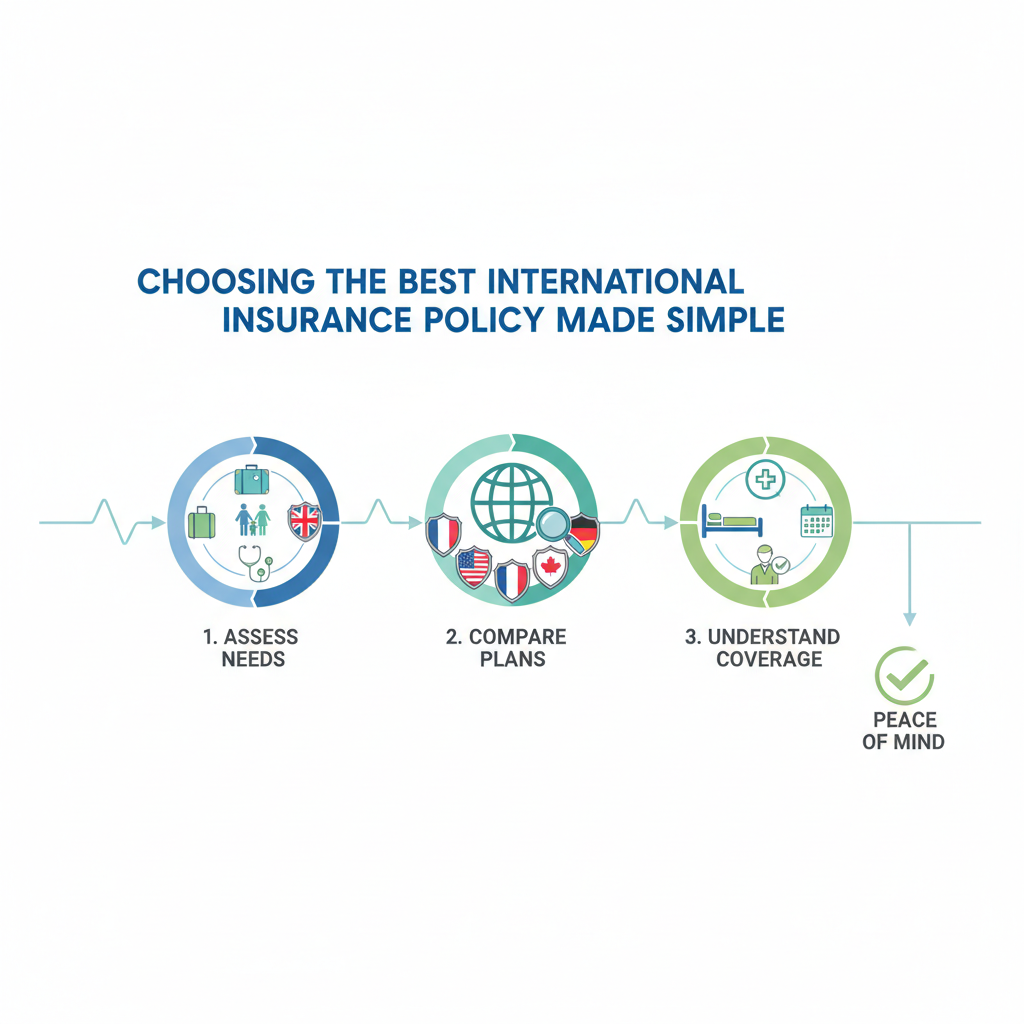

Understand Your Personal Needs

The first step in choosing the best international insurance policy is understanding your specific requirements. Ask yourself key questions: How long will you be abroad? Which countries will you visit or live in? Are you traveling alone or with family? Do you have pre-existing medical conditions? For example, a short-term traveler may only need basic travel insurance, while an expatriate or student will require long-term international health insurance with broader benefits.

Evaluate Coverage Options Carefully

Coverage is the heart of any insurance policy. A good international insurance plan should include inpatient and outpatient care, emergency services, hospitalization, and prescription medications. Some policies also offer maternity benefits, mental health coverage, dental care, and vision services. It is important to review what is included and what is excluded. Pay close attention to limits, deductibles, and co-payments, as these directly affect how much you will pay when making a claim.

Check Geographic Coverage

Not all international insurance policies offer worldwide coverage. Some exclude specific regions or countries, often due to higher medical costs. For example, coverage in countries with expensive healthcare systems may require an additional premium. Make sure the policy covers all the destinations you plan to visit or reside in. If your plans change frequently, opt for a policy with flexible geographic coverage to avoid gaps in protection.

Compare Premiums and Value

While cost is an important factor, the cheapest policy is not always the best choice. Instead of focusing solely on the premium, consider the overall value. A slightly higher premium may provide significantly better coverage, faster claims processing, and access to a wider network of healthcare providers. Balance affordability with the quality and extent of coverage to ensure long-term benefits.

Understand Policy Exclusions and Conditions

Every insurance policy has exclusions, and international insurance is no exception. Common exclusions include cosmetic treatments, elective procedures, injuries from high-risk activities, and certain pre-existing conditions. Some policies may cover pre-existing conditions after a waiting period, while others may exclude them entirely. Reading the policy terms carefully helps avoid unpleasant surprises during claims.

Assess the Provider’s Reputation

The reliability of the insurance provider is just as important as the policy itself. Choose a provider with a strong international presence, good customer reviews, and a solid track record in claims handling. Efficient customer support, especially multilingual assistance, is crucial when dealing with emergencies in foreign countries. A reputable insurer ensures smoother communication and faster resolution of issues.

Look for Additional Benefits

Many international insurance policies offer added benefits that enhance convenience and security. These may include 24/7 emergency assistance, telemedicine services, wellness programs, and coverage for emergency evacuation or repatriation. Such features can be invaluable during critical situations and add significant value to your policy.

Review and Update Your Policy Regularly

Your insurance needs may change over time due to relocation, family additions, or changes in health status. Reviewing your policy annually ensures it continues to meet your requirements. Updating coverage when necessary helps maintain adequate protection and prevents underinsurance or unnecessary expenses.

Final Thoughts

Choosing the best international insurance policy does not have to be complicated. By clearly identifying your needs, carefully reviewing coverage options, understanding exclusions, and selecting a reputable provider, you can secure a policy that offers reliable protection worldwide. International insurance is more than just a financial product—it is an investment in your safety, health, and peace of mind. With the right approach, you can confidently navigate global opportunities knowing you are well protected.

Leave a Reply